Most of you have seen the video about the Crazy Nastyass Honey Badger, with narration by Randall, somewhere in your travels around the internet. I delight in using the honey badgers to teach about crisis hotlines; we’re using the honey badger in our initial training to talk about inappropriate sexual callers, frequent callers, the virtues of directness, etc.

Today I’d like to talk about language. At one point, Randall says “Oh, the honey badgers are just crazy!”. There could hardly be any moment more germane to start our discussion of pathologizing language.

What is pathologizing language?

I’m thrilled that you asked. It’s judgmental language that examines someone’s behavior and ascribes a pathological cause to it. In plainer English, pathologizing language assumes that others are the way they are because they’re sick, and (by inference) makes the sickness seem like the most important thing about the person.

“The honey badgers are just crazy!” labels the honey badger with a mental illness and basically says that you don’t need to know anything else about them–they’re just crazy; what else is there to know? It’s a label that puts the honey badger in a box and assumes that we, the outside observers, are capable of knowing exactly what is going on for the honey badger and why it behaves the way it does.

We might just as fairly say that honey badgers are highly adapted predators with little fear of pain. They’re courageous and resourceful, fierce and dangerous. They’re really good at doing what comes naturally for them: being total badass predators you would not want to meet in a dark alley.

But that’s not the same as being crazy. When we call them crazy, we’re using a stigmatizing term from our experience that makes their natural behavior (badass predator mode) seem like an illness or like there’s something wrong with them. That’s pathologizing language.

Examples of pathologizing language

People often use pathologizing language as part of an ad hominem attack designed to undermine a person’s credibility or standing. By associating another person with something we find undesirable or sick, we subtly damage the other person. Often we include minimizers like “just” or “only” to help the knife sink even deeper.

“She’s just a crazy person”

“Yeah, he’s an alcoholic, what do you expect?”

“Oh, she’s PMSing again, it’s always like this around this time of the month”

“Stop acting so gay”

“Just another entitled homeschooler”

“You’re just suicidal”

“Of course he has health problems… he’s fat”

“I mean, she’s an engineer. Why were you expecting empathy?”

“She’s such a drama queen”

“We got another whiny schizophrenic on line 2”

In each case, we’re applying a label and using it to minimize and disrespect how the other person is feeling. We also make it seem as though the person’s behaviors and feelings are due to some problem that we’ve identified. We’re assuming that we know why the person is doing what they do, and are therefore writing it off. That’s the real problem with pathologizing language: it covers up disrespect and allows us to pigeonhole people and forget about them.

What if there really is a problem we need to discuss?

Non-pathologized honey badger (c) Hollis Easter

Sometimes we still have to talk about stuff, and sometimes people really do have mental illnesses, suffer from addictions, or behave in ways that society has decided are inappropriate. When that’s the case, use non-pathologizing language wherever possible.

What’s non-pathologizing language? It’s not making assumptions about what causes a person’s behavior, not pigeonholing them, and not claiming that you can know everything about a person just because you know some labels for them.

This can be subtle; here are some examples:

The honey badgers are just crazy. (pathologizing and belittling)

The honey badgers are mentally ill. (pathologizing; defines what the HBs are)

The honey badgers have mental illnesses. (less pathologizing; reports the fact but not as the only thing about them)

The honey badgers are living with mental illness. (less pathologizing; reports the fact but draws attention away from it)

The honey badgers suffer from compulsive behaviors. (even less pathologizing; reports what they do, in a compassionate way)

The honey badgers hunt cobras even when they aren’t hungry, and they seem unable to stop. (even less pathologizing; focuses almost totally on what they do.)

More?

Mrs Honey Badger is PMSing again. (pathologizing)

Mrs Honey Badger seems very angry today. (non-pathologizing)

I wish Mr Honey Badger would stop acting gay all the time. (pathologizing)

I get confused and uncomfortable when I see Mr Honey Badger looking for new cobra recipes in cooking magazines. (non-pathologizing; gets at the root of the speaker’s concern)

We could go on, but in general:

Describe what you see, not what you think it means. If someone is talking to people who aren’t visible to you, say that–there’s no need to say it’s because they’re crazy or because they’re schizophrenic.

Talk about behavior, not what you think caused it.

Beware of using language that minimizes other people’s experiences or encourages them to be silent.

Recognize that what you think is aberrant and sick may just be normal behavior for other people. Stay open to that possibility.

The honey badgers get sad when people call them crazy. They’re just trying to be themselves, working their way through a confusing and changing world that’s full of cobras and jackals that steal their mice and call them stupid.

Before you read the rest of this, watch this video of a Russian mouse with a great attitude:

That mouse would be a failure in most schools.

Unless they’re using something like standards-based grading (SBG) that allows students to reassess skills that they didn’t ace the first time, most schools and universities don’t value performance that’s preceded by failure. We expect excellence the first time, we select for it, and we punish people who don’t measure up. So even though the mouse eventually got the biscuit, it doesn’t matter because it’s only the first attempt that counts.

Sadly, that mouse would also be a failure in most workplaces.

Unless they’re unusually progressive, most offices expect 100% success from employees and have little tolerance for failure. We expect external failures—places where the outside circumstances didn’t go our way—but have no room for internal failure. Even if it’s a new project that nobody’s ever done before, we expect wins and punish losses. Failing at a task is dangerously close to being a failure, and nobody wants to be a failure.

This leads to risk aversion. Most of us wouldn’t bother even trying to steal the cookie, because it looks too hard and the probability of failure is pretty high. The costs of failure are huge. The costs of not even trying are pretty low. So we don’t try.

But what happens when you watch the mouse?

You want it to succeed. It’s agonizingly close to getting the biscuit, but then it gives up. Apparently. Or maybe it’s just sitting there on top of the shelf, looking at things from a new angle. After a protracted space of time spent motionless, the mouse jumps back down, grabs the cookie, and nails it on the first try. It learned something from those initial failures and it succeeded in the end.

Thoughts

Why do we care so much about initial success? Why do we give it so much weight in our estimation of value? The fixation isn’t universal—everyone knows that you have to throw a lot of basketballs, play a lot of scales, and draw a lot of stick figures before you get very good at sports, music, or art—but it’s still prominent.

Think of five things in your life that you do really well. Could be part of your profession (counseling people in pain, calculating amortization, making proper Hollandaise sauce, driving an 18-wheeler, writing a grant proposal) or part of your home life (getting out stains, changing diapers, making dinner, fixing clogged toilets, hosting parties) or something to do with a hobby (throwing bullseyes in darts, climbing mountains, making beaded necklaces, making great beer, skiing black diamonds) or whatever else comes to mind.

How many of those five things did you do really well from the beginning? Did you have initial success in any of them? I didn’t. I got in trouble for not practicing music, was told that I couldn’t draw, was called ungraceful and fat and ugly and not welcome in dance class, burned my first attempt at chocolate sauce, fell on my face when trying to skate, accidentally erased some important computer disks back when 5.25″ floppies were the norm… you get the idea. Not a lot of initial success for me.

How many of us are still seeing the first person we ever kissed? Doing the first career we tried?

I was reading Malcolm Gladwell’s Outliers last night, and he talks a lot about how most truly excellent practitioners are people who received a ton of opportunity for practice early on—they got a chance to earn their 10,000 hours of practice on the way to expertise. It’s an excellent point, and the thing I want to add is this: most of the outliers he talks about failed at things. A lot. They just had the opportunity to keep trying without being punished for it.

They were mice that had a chance to practice long enough to get the biscuit.

Goals

Let’s start by trying to notice the places in life where we fall into the initial success model. There are spots where we afford equal weight to later successes, and there are spots where initial success is so important that we shouldn’t change our habits (as the saying goes, “if at first you don’t succeed, don’t take up skydiving”).

But I wonder how things would change if we adopted more of a growth mindset and looked more at the outcomes and less at the path and time it took to reach them.

I’ve long believed that the truest measure of a teacher comes not from their star students but from their middling ones. The really good students—the ones who succeed on their first try—probably will do pretty well with any teacher. But the middle ones require more help before they get it, so they’re a better way of seeing how well a teacher teaches. They’re the mice that fell a bunch of times but still got there.

Next time you’re teaching, try to look for the future cookie-robbing rock star mice inside your students, and see whether you can let go of initial success long enough to help them find the goal a little later. As with so many things, after a while “who got there first?” stops feeling so important, and what really matters is what we do once we all arrive.

People use savings accounts for the wrong thing, and it hurts them.

Every bank I’ve seen has savings accounts, and they all come with snazzy logos and slogans like “Watch your savings grow with HSBC!” or “It all starts with saving today” or whatever. The banks pretty much say that if you sock money away into savings accounts, you’ll be rich somewhere down the line. The problem is that it isn’t true. Far from being get-rich quick schemes, savings accounts, used badly, are basically guaranteed to help you get poor slowly.

A savings account is a really safe bet. It’s one of the few places where you can store money and be legally guaranteed to get it all back at the end. The only problem is that the money from the savings account isn’t worth as much when you get it back.

Wait, what? That doesn’t make any sense at all! If you got all the money back, how is it less valuable?

Because inflation–the tendency of prices to rise over time–means that the buying power of your money fades away unless it grows faster than prices are going up. Unless your savings account reliably pays a higher-than-inflation interest rate, which almost none of them do, you’re losing money over time. That’s a problem if you’re thinking of a savings account as a way to grow your money.

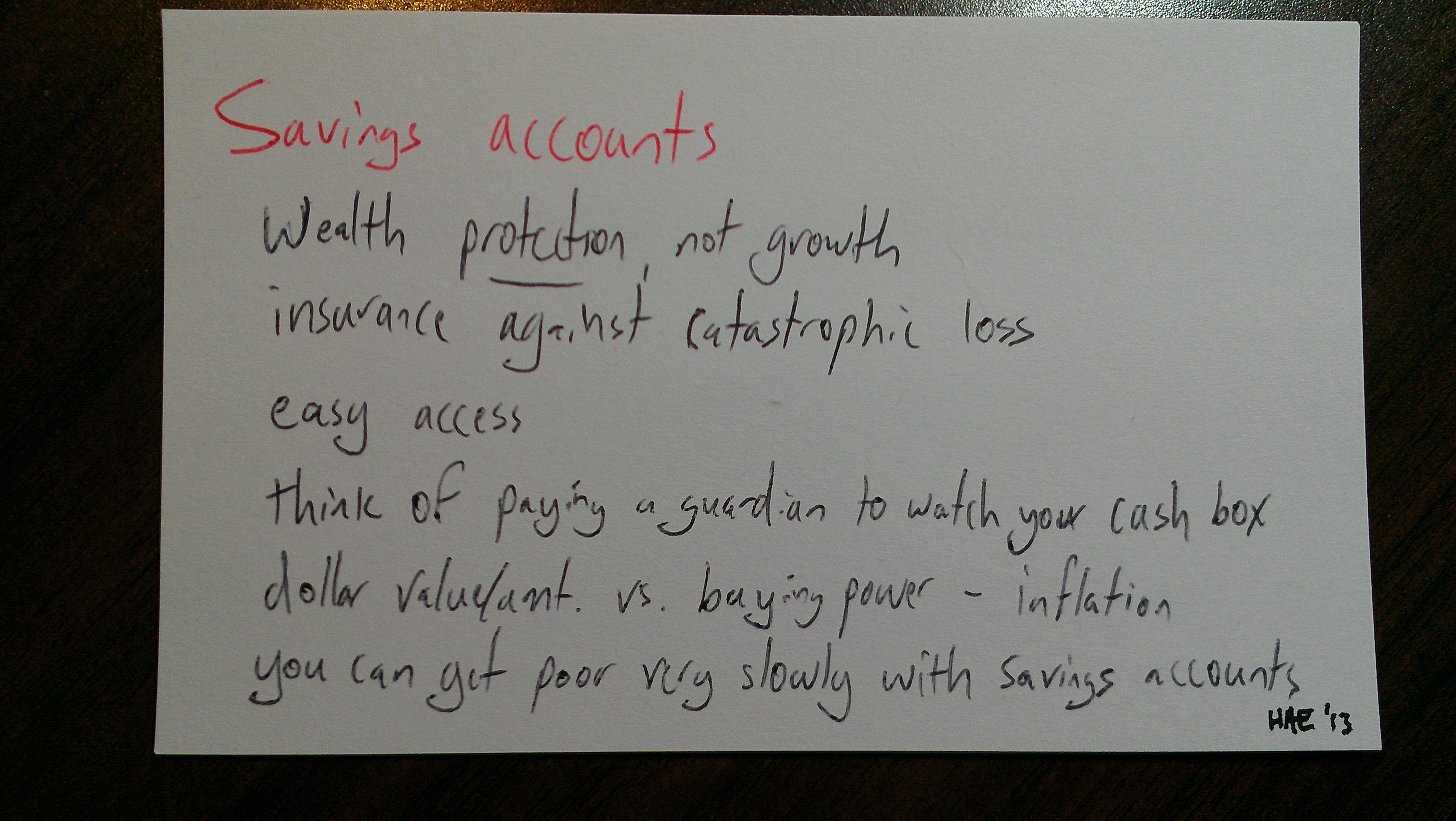

I’d like to encourage you to think about savings accounts differently. They have a place, but they aren’t about growing your wealth. Savings accounts are for protecting money you might need to access quickly someday, not getting more money. Think of your savings account as an insurance policy, not an investment, and you’ll be on solid ground.

Are your eyes glazing over? Don’t worry! People use lots of abstract words to talk about money, and I think it confuses things and makes normal people throw their hands up and just continue making poor choices because it all feels too complex and hard to understand. So I’m going to try to use plain English as much as possible, with concrete examples and drawings on index cards!

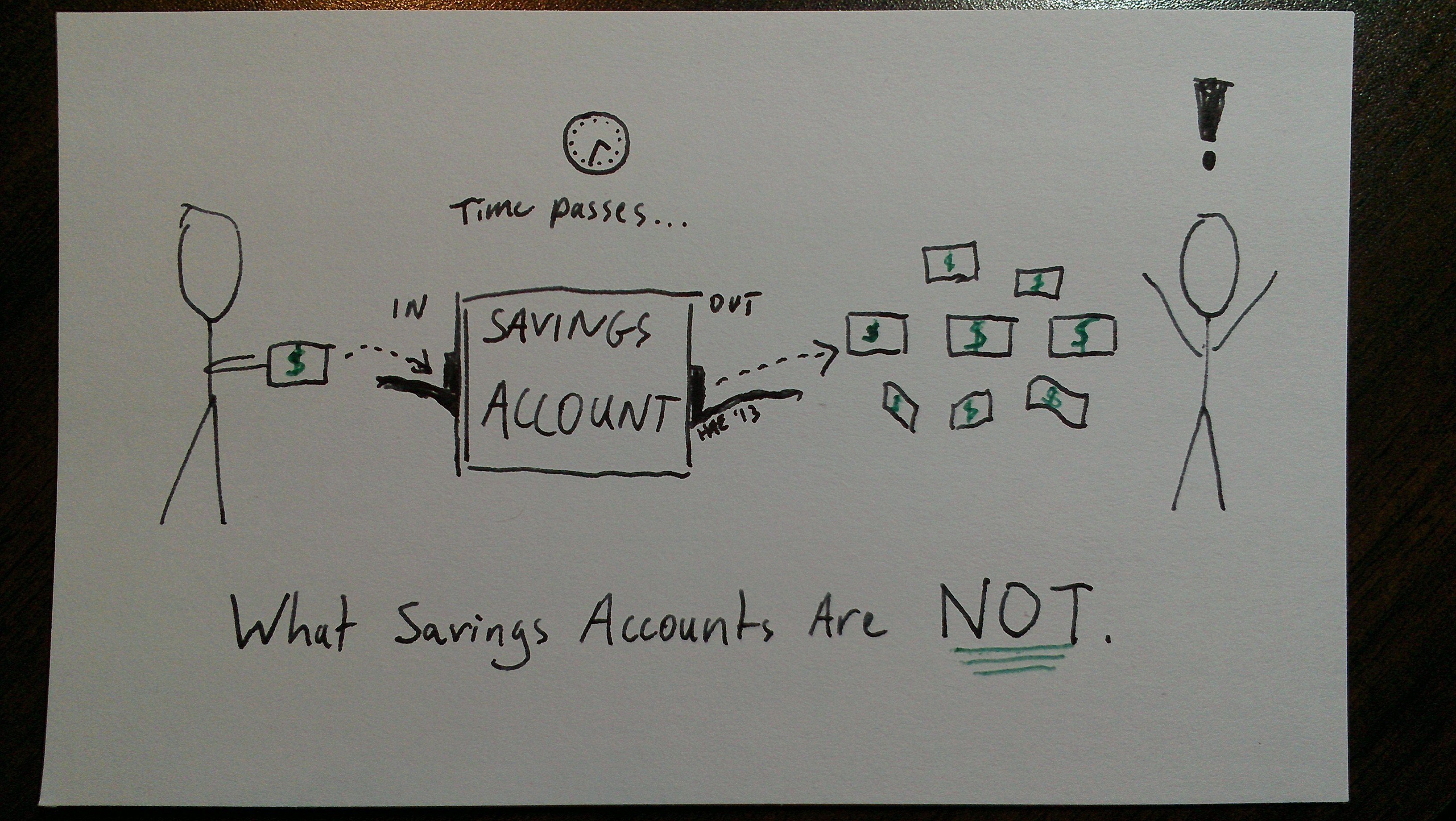

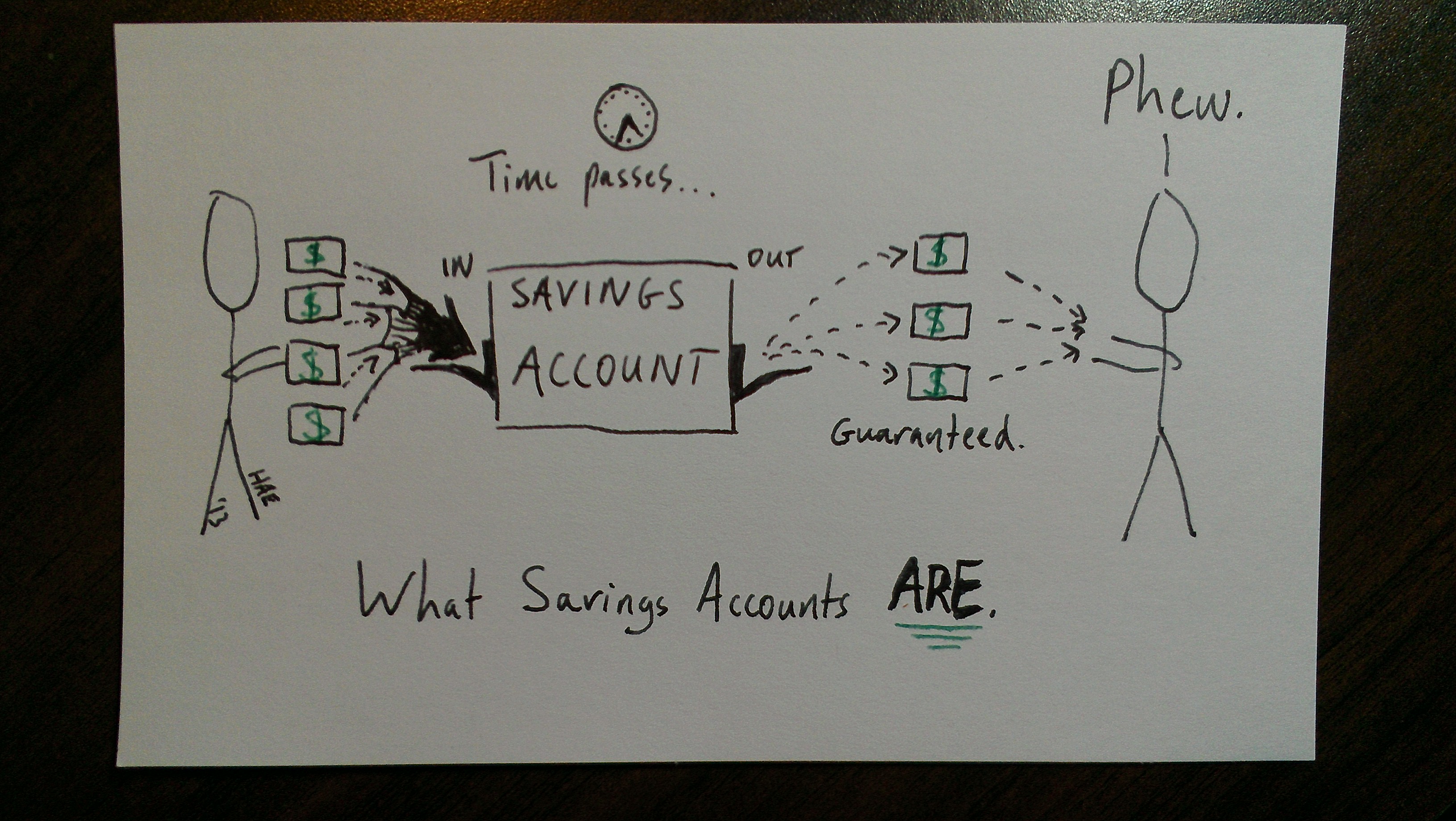

What savings accounts are not

What savings accounts are not (c) Hollis Easter

Savings accounts mostly don’t grow in value over time. I want to be able to talk about a couple of concepts here, so let’s define some terms.

Value is a measure of what I can do with some money: if I want to buy a new set of bagpipes or have someone repair my furnace, I need enough value that someone is willing to trade their stuff for my value.

Dollars are units of US currency. They’re related to value, but they aren’t the same, because a given number of dollars won’t always buy you the same amount of stuff. Think about how Red Sox tickets cost a lot more during the World Series than during pre-season, or about how gas used to cost $0.85 per gallon and now costs $3.92.

Inflation is a name for the observed trend that, as time passes, you need more dollars in order to reach a certain amount of value. When I bought my first cup of coffee, it was less than a dollar; now, a cup of coffee from the same store costs $2.25. That’s inflation.

Back at the top of this section, I said that savings accounts mostly don’t grow in value over time. What I mean is that although the number of dollars in your savings account will grow over time, it won’t grow as fast as inflation, and that means that the value of your money–what you can do with it–tends to shrink over time.

Want some proof?

If you’re bored by numbers, skip this section. Otherwise, read on.

You can look up historical US inflation rates at the Bureau of Labor Statistics’s Inflation Calculator and use it to calculate annual inflation. What they call “buying power” is what I’m calling value.

I’ll go year by year, since that makes the inflation easier to see and ties nicely into the discussion about interest rates that we’re going to have in a moment. Imagine that you’ve taken $1000, stuck it under a mattress, then come back the next year to buy something with it. Unfortunately, all the prices are higher now.

2007: You’d need $1028.48 to buy what used to cost $1000. (2.84% inflation).

2008: You’d need $1038.40 to buy what used to cost $1000. (3.84% inflation).

2009: You’d need $996.44 to buy what used to cost $1000. (-0.36% inflation). This was the big crash year.

2010: You’d need $1016.40 to buy what used to cost $1000. (1.64% inflation).

2011: You’d need $1031.57 to buy what used to cost $1000. (3.16% inflation).

2012: You’d need $1020.69 to buy what used to cost $1000. (2.07% inflation).

2013: You’d need $1019.84 to buy what used to cost $1000. (1.98% inflation).

That’s what I mean when I say your money loses value over time. Unless your number of dollars grows faster than inflation, your money buys less later on.

But what about interest?

Good question. Most banks offer interest on their savings accounts, which entices you to put in more money. Think of interest rates as advertising tactics; they’re tools for convincing you to put money in the bank (which will then make it grow for itself by investing it other ways). Earning interest on accounts is good, but you’ll notice that banks almost never offer rates that beat inflation. Here’s a quick survey of some banks I know, ranked from highest to lowest:

2012-2013 inflation rate: 1.98% (banks have to beat this to beat inflation)

Capital One 360 Savings: 0.75%

First Niagara Pinnacle Money Market: 0.2%

Citibank Savings Plus: 0.15%

HSBC Premier Savings: 0.15%

HSBC Advance Online Savings: 0.05%

Commerce Bank myRewards Savings: 0.03%

Key Bank Personal Saver: 0.02%

First Niagara Statement Savings: 0.01%

You’ll notice that all the banks offer way less interest than what it would take to beat inflation. Some of them are just ridiculous!

The best of the ones I listed (Capital One 360 Savings) would earn you $7.50 on your $1000 savings in one year, which means you lose $12.34 in value because of inflation. The worst of them (First Niagara Statement Savings) will pay you a whopping ten cents on your $1000. At that rate, if you wanted to buy yourself a cup of Starbucks coffee ($2.75) with your annual interest earnings, you’d have to put $27,500 in the bank for a year!

Turning back to inflation, the bigger problem is that your $1000 is now worth a lot less. Remember that you need $1019.84 in 2013 to buy what $1000 would have bought in 2012. So even if you’ve got that sweet Capital One 360 account, you still only have $1007.50 and you need $1019.84, so you’ve got to come up with that extra $12.34 out of your pocket if you want to buy something. And we aren’t even talking about taxes on the interest yet!

Interest rates are marketing and advertising tools designed to convince you to lend your money (they’ll call it ‘deposit’ or ‘save’) to a particular bank. The banks can have lots of reasons for wanting to do that, but basically it comes down to cash flow: they’ll take your money, lend it to other people, invest it to make more money, or hold onto it to secure their own debts. They’ll pay you a little bit (the interest) for letting them hang onto your money, but unless they’re paying you a rate higher than inflation, your money isn’t growing.

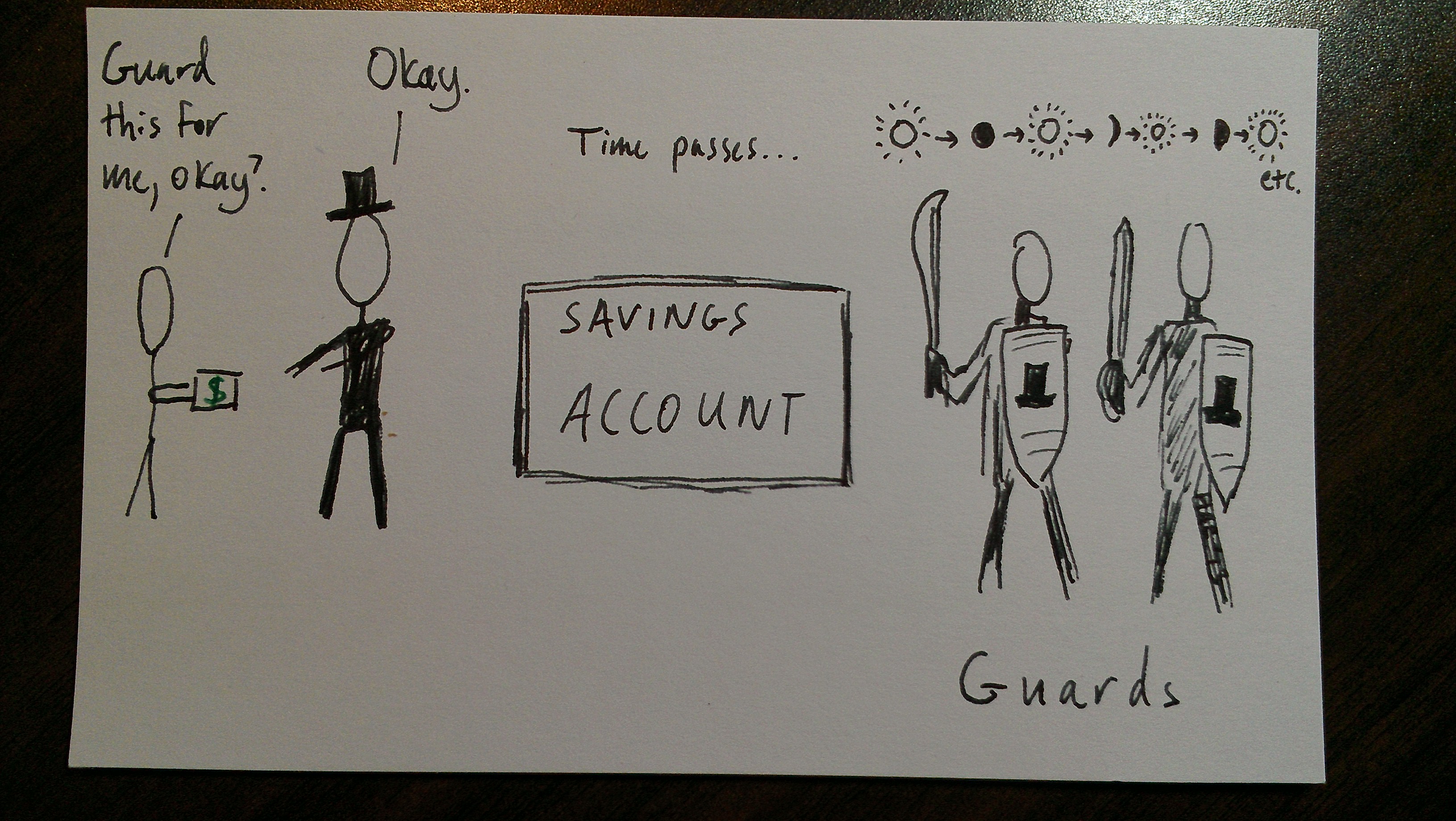

Hiring yourself some guards

I’ve been talking a lot about how savings accounts are unhelpful for making your money grow, and you might be wondering: “what’s the point of having a savings account at all?”. Savings accounts are great tools for making sure that you have access to your money, immediately, whenever you need it. In financial terms, they have very high security (your money is guaranteed to be there) and liquidity (you can have it immediately just by asking).

Savings accounts are for your emergency fund: the money you’ll need immediately if you lose your job, your house has a catastrophe, or someone in your family has an accident and needs immediately medical care. When these things happen, you need the money to be there, and you need it to be there Right Now.

You don’t want to keep the money in your house: someone could break in and steal it, or your house could burn down, or a tornado might carry it away. You want something more secure, so you decide to hire some guards to look after your emergency fund.

You head down to Top Hat National Bank and make an agreement with the banker: he agrees to protect your money 24/7, guaranteeing that he will give it back to you whenever you ask. He takes your money and puts it in the savings account, which is guarded night and day by hulking Myrmidons in suits of armor.

Hiring some guards (c) Hollis Easter

This is fantastic! Totally secure, and now your emergency fund is really safe. Mr Top Hat wants to be paid something for his efforts–all those guards want a paycheck too–but you’re happy to pay it because you value being able to trust that your money is safe and immediately available, forever.

You feel even safer knowing that Mr Top Hat’s promises are backed by the full faith and credit of the US federal government thanks to FDIC and NCUSIF/NCUA–the insurance policies that banks and credit unions have to buy before they’re allowed to guard your money.

So you choose the savings account because, even though its low interest rate means losing ground to inflation every year, the advantages outweigh the costs. You’re basically buying an insurance policy against catastrophic loss, and you’re paying for it by losing a little money to inflation.

This has nothing to do with investing or growth. The purpose of the savings account is to protect a portion of your money so that it will always be there when you need it, no matter what.

What savings accounts are (c) Hollis Easter

The bottom line

You’ve probably noticed that the only difference relates to your intentions.

If you’re saving money because you want it to grow, you’re going to be disappointed by a savings account. You’re using the wrong tool for the job; you’ll need to look into investing in things like stocks or bonds if you want to end up with substantially more money than you started with. Inflation matters here.

If you’re saving money because you want to protect it and make sure it’s there in an emergency, a savings account is an excellent choice. You’re willing to pay the Myrmidons to guard your cash, and the insurance they provide is valuable to you. This is a great way to secure your emergency fund. You don’t care about inflation here; you care about security.

I’m not saying that you should stop using savings accounts–far from it! Some of your money should always be in savings, for the emergency fund we talked about. Folks differ about how much money they want to have in emergency funds, but most people say anywhere from two weeks to a year of living expenses. That’s money that you really can’t afford to lose, so it goes into a savings account.

Once you’ve got that amount safely stocked away and guarded by the metaphorical Marines in Fort Top Hat, then it’s time to think about investing some of your money to make it grow. Savings accounts are the wrong route for this money–you need investment.

Any questions? Please leave a comment! If this was helpful, please share it with your friends!

Savings accounts summary (c) Hollis Easter

Disclaimer: I’m thinking about systems here, and that leads to some hand-waving that’s a little confusing about who’s getting paid what. The bankers aren’t getting paid by inflation, exactly, so it’s not accurate to imply that the banks are getting rich directly because your money isn’t keeping pace with inflation. However, I’m in the metaphors business, and the guards needing to be paid is a much more useful metaphor than the degree to which the returns offered you by the bankers based on the investments they’re making with your lent capital are keeping up with rising consumer prices and losses to tax.

The point here is that I’m trying to help you see savings accounts in a different light, which I hope this framing achieves. Also, I encourage you to read and think about this stuff on your own, but I am not a financial advisor and don’t know your situation, so I can’t guarantee any particular outcome for you. That should take care of the legal disclaimer fine print, eh?